General Aggregate Limits: A Potential Insurance Risk Hiding in Plain Sight

Read more on our Blog

In the process of hiring a new vendor, you review their certificate of insurance (COI) to make sure your company is covered against a potential loss:

- The Commercial General Liability (CGL) policy is active and coverage amounts are ample for the project’s value.

- The vendor has workers’ compensation insurance.

- The COI cites your company as an additional insured.

Everything is good to go, right? Not so fast. A liability cap may be hiding in plain sight known as the “general aggregate limit.” Understanding when this limit takes effect can mean the difference between a vendor having coverage or being underinsured. This article details the three different applications of the general aggregate limit and some common pitfalls that impact coverage.

What is the General Aggregate Limit?

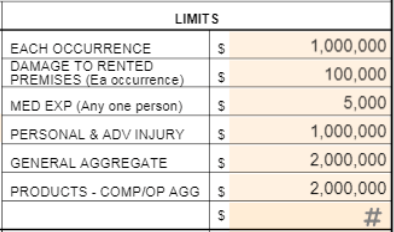

CGL insurance policies carry liability limits, which means that during the term of coverage, the insurance will pay only up to a certain amount. Once the policy reaches those thresholds, its financial resources are exhausted. Two important limits include “each occurrence” and “general aggregate”:

Each occurrence is the maximum amount a policy pays for an individual claim. Using our example limits, this policy pays up to $1 million for a single claim but cannot exceed that amount. Overages must go toward an umbrella or excess insurance policy or result in out-of-pocket costs.

General aggregate represents the maximum amount a policy pays out across all claims. After paying $1 million for the example claim above, the policy still has $1 million remaining to cover any additional claims during the coverage term.

When do General Aggregate Limits Apply?

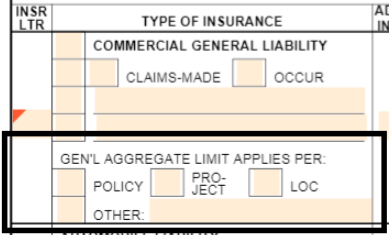

Understanding how limits impact payouts is step one. Next is knowing when the limits apply. This information comes from the three boxes under “General Aggregate Limit Applies Per” on the COI.

Policy indicates that the limits apply to the insurance policy in total. A vendor may work on several projects at once for different companies under the same policy. Should the vendor cause losses at different worksites, all claims go against the general aggregate as a whole. After reaching $2 million, the policy stops paying. Companies filing claims after the aggregate is reached likely will not receive payment.

Project applies the liability limits to each job rather than the entire policy. Therefore, our vendor would have $2 million in coverage for each project. If the vendor did five projects per year, they have a policy aggregate of $10 million in coverage. Project is a preferred general aggregate for hiring companies because it provides a higher coverage threshold and more control over that money. Should another company file a claim against the vendor’s policy, the amount of that claim would have no bearing on how much the policy would pay against any other losses filed under a separate project.

Location applies only to the properties owned or rented by the policyholder. This aggregate limit has no application for a company hiring a vendor because it excludes worksite locations. The location limit is designed only for the named insured’s properties like office buildings, retail locations, and equipment storage facilities.

What are Some General Aggregate Limit Pitfalls?

- Know how courts define an occurrence – Courts are divided in what constitutes an occurrence. Let’s say our vendor is an electrician whose faulty work causes a fire injuring 20 patrons. Some state courts apply the “cause test,” which views the liability cause as the faulty wiring. This equals one occurrence. Other state courts apply the “effect test.” This method defines the occurrence by the resulting damage or injury. In this case, the court considers each injured patron a separate occurrence for 20 total claims.

- Check for project aggregate endorsements – Simply checking the project aggregate limit box on the COI does not mean the coverage exists. Per project is not standard and often comes with an additional premium cost. The CGL policy requires a per-project aggregate endorsement that should be attached to the COI upon submission to verify accurate coverage.

- Beware CGL policy extensions – Policyholders sometimes seek to extend their policies for longer than the standard 12 months but less than an additional full term. Perhaps a project will last 15 months, so a vendor gets a three-month extension of their CGL policy. Know that when this happens, the aggregate limits do not reset at the 12-month mark. The aggregate extends for the 15 months increasing the likelihood that the amount could be exhausted. Note the effective and expiration dates of the policy on the COI to identify this potential issue.

Do not Let General Aggregates Limit Your Project Protections

If your business could benefit from an automated system for tracking and managing certificates of insurance, schedule a demo with illumend, from myCOI. Our platform is built on industry logic and supported by insurance experts. The software tracks each important detail of COIs to keep your company safe. When it comes to risk, we erase the worry and save time so you can get back to work.

The next uninsured third-party partner won't announce themselves.

illumend catches the gap.

You save the project.

Blog & Insights

What Are Policy Limits?

What Is Insurance Renewal Tracking?

What Are Insurance Requirements?

What Is an Insurance Exclusion?

Moving Beyond Spreadsheets to Manage Construction Risk

myCOI Launches illumendTM: Smart, Fast, Confident Compliance—Just a Click Away

Compete in a Crowded Industry with the Right Insurance Technology

General Contractors NEED Automated Certificate of Insurance Software

Has Your Organization Been Hurt By Insurance Claims?

Construction Industry Trends For Additional Insureds

.jpg)

How Insurance Agents Can Achieve Clients For Life

Get Your Team Off Your Back About COI Tracking

You Could Be Saving 30% on Insurance Tracking Costs

Tip# 1 – The “INSURED” Box

Constructing A Strong Contract

Are You Really an Additional Insured?

Insurance Agents: Watch Your Client Base Grow

What You Need to Know About Certs and Real Estate

Insurance and Cannabis: What You Need to Know

Create a Unique Agency Sales Strategy with myCOI

Important Steps for Managing Risk Using Your RFP

Cybersecurity and Remote Work: Managing the Risks

Blanket Endorsements: The ‘Am I Covered’ Checklist

10 Tips for Transferring Contractual Risk

myCOI Gives Back to the Community

A Guide to myCOI’s Go-To Insurance Resources

Here’s What You Need to Know About Example COIs

When You Need a Sample COI, Think ACORD

Here’s What You Need to Know About COIs

Insurance Compliance Will Be a Critical Role in 2022

.jpg)

Always, Always Remember that ACORD is not an Insurer

Agents: Your Insureds Deserve Automated COI Tracking

The Right Compliance Management Software is Crucial

The ABCs of Certificate of Insurance Compliance

A COI Template Will Only Take You So Far

The Importance of A Signed Contract

Checking More Than Just Expiration Dates

Dominate Your Insurance Agency Earning Power

Additional Insured Updates You Need to Know

Is COI the same as liability insurance?

The Basics of Quarterly Tracking

The Basics of Additional Insured Endorsements

What Is a COI in Contracting?

What Is A Certificate Of Insurance (COI) For?

Primary and Noncontributory Endorsement Form

7 Strategies for Managing Insurance Renewals

Fraudulent Certificates of Insurance Present Real Risks. Are You Prepared?

General Liability Certificate of Insurance

Certificate of Property Insurance

How to Check If a Business Has Insurance

How do I get an insurance certificate?

Customer Asking for Certificate of Insurance

How Do I Get a Certificate of Insurance in the USA?

The Basics: Waiver of Subrogation

What Is A Surety Bond and Why You Need One

You Need MORE Than Just Holding COIs

The Wrong COI is Just as Bad as No COI

It’s Easy to Create Your Own COI. Don’t Do it.

5 Things to Do to Verify Your COI is Valid

Finding a Certificate of Insurance Online is a Risk

Premiums Are On the Rise

A COI Example Can be a Great Guide—Or a Burden

Contractors Pollution Insurance

COI Real Estate

Broker Certificate of Insurance

Building Certificate of Insurance

What Is An LLC Certificate of Insurance?

Who Is Responsible for Subcontractors’ Work?

Do Contractors Need Insurance?

Construction Insurance Risk Management

Subcontractor Default Insurance: Everything You Need To Know

How Do You Calculate Building Construction Coverage?

What Is Regulatory Compliance in Construction?

What Is Not Usually Covered by Building Insurance?

What Is the Difference Between Property Insurance and Builders Risk Insurance?

What Is Considered a Third-Party Insurance?

What Is a COI in Construction?

Types of Construction Insurance

Why Is Builders’ Risk Insurance so Expensive?

What Is Builders’ Risk Insurance?

Third-Party Insurance Verification

Why Should I Outsource COI Tracking to myCOI?

Insurance Tracking Services

How Can You Track Insurance Policies?

What Is Insurance Certificate Tracking?

How to Ensure Contractor Compliance

myCOI Expands Procore Integration to Simplify Compliance and Payments

How Do I Generate a Certificate of Insurance?

Why Does a Company Need a Certificate of Insurance?

What Is an Insurance Certificate for a Business?

.jpg)

How Much Does a COI Cost in the USA?

How Important Is a Certificate of Insurance?

What Are COIs? A Guide To Certificates of Insurance

Agents: Help Contractors Manage Insurance Risks

What Is COI in Risk Management?

What Are the Five Elements of Risk Management?

What Is a Third-Party Risk Management System?

What Are the Key Elements of Third Party Risk Management?

Compliance in the Construction Industry

Third-Party Risk Management in Construction

You don't have to understand insurance to be good at insurance compliance.

With Lumie™, compliance is covered. So is everyone on your project.

Get The Lantern

.avif)