It’s Difficult to Quantify Social Inflation, But it’s Crucial to Comprehend

Read more on our Blog

Social inflation affects our industry in big ways, but many of us don’t understand what it is or how it’s doing it. Here, we’ll break social inflation down, discuss it, and gain an understanding of what we can do as an industry to combat it.

What Social Inflation Is

In addition to general economic inflation, social inflation captures how insurance companies’ claim costs can rise above general economic inflation coupled with societal preferences over who should absorb risk. Insurers can modify pricing models or loss reserves to mitigate general economic inflation, which is caused by unpredictable factors such as rising expenses. Social inflation, on the other hand, may result from a variety of different factors and is harder to hedge bets against.

The impact of these and other issues in the legal landscape can be intensified by third-party litigation funding. Factors that can affect social inflation include longer legal proceedings, tort reforms (or rollbacks therein), mistrust of corporations, emotionally charged jury trials, and an increase in the number of extensive jury awards. The social nature of this form of inflation implies that the public is growing more skeptical of business, and more pointedly, large corporations; this is allowing for more of a sympathetically-leaning juror landscape.

What the Effect of Social Inflation Is

When social inflation occurs, insurers pay out higher claim amounts and loss ratios which drives up policy costs. An inflation rate like the Consumer Price Index (CPI) may be used to compare the impact of social inflation components on claim losses over time with inflation. Social inflation can’t be measured by standard means like the CPI.

Commercial automobile, professional liability, product liability, and directors and officers liability are just a few of the insurance lines that are most vulnerable to social inflation. However, private passenger automobile insurance appears to be under pressure as well. This doesn’t mean that other lines of insurance aren’t affected, but rather the social pressure in these lines is higher as per the previous section where we discussed how public sentiment toward big business is changing. Let’s talk about that a bit more.

One of the more interesting things to come from this is newer juror tactics used in court cases to play more heavily on the emotions surrounding safety and survival, often referred to as “Reptile Theory.” Humans tend to side with things we find that help us with our own survival. Employing empathic devices, a lawyer can leverage Reptile Theory to put the jurors in the shoes of someone else. By doing this, defendant payouts have increased because jurors see themselves as the plaintiff. This has led to a desensitization to massive awards due to the media playing these up. Social pressure comes from this, thus social inflation creeps in.

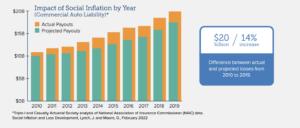

This graphic from iii.org shows the impact social inflation is having on the industry.

What is Driving Social Inflation?

An investor providing money to attorneys or clients in return for a financial stake in the outcome of a legal case or arbitration is known as third-party litigation funding (TPLF). This kind of funding is usually described as a non-recourse loan because it does not have to be repaid if a case is lost or dismissed. Non-recourse loans are also known as legal funding, third-party litigation funding, and alternative litigation funding (ALF). This fast-growing multibillion-dollar industry, valued at $17 billion and predicted to reach $30 billion by 2028, is increasing and is adding to the social inflationary environment we live in today. It’s essentially gambling on court cases, and it’s legal.

According to research, TPLF can cause social inflation by allowing for longer litigation, making insurance coverage more expensive. There are several other aspects of TLPF that may cause problems. The hedge funds behind many of these TPLF efforts operate without disclosures and safeguards and can keep the litigation going in hopes of their side winning.

So What Can be Done?

When social inflation occurs, there are a few things that you can do to control it. First, you can try to tailor the risk profile of your customers so that all of them pay roughly the same amount. If you can’t do that, you can try to separate customers by certain factors like age, sex, or location to create artificial differences in the risk profile of your customers so that they are all paying roughly the same amount. If these options don’t work, you can also try to lower your own costs by improving the quality of your service. This can be achieved by simplifying your policies, automating specific processes (like how you collect and analyze the mountains of certificates of insurance), improving the accuracy of your data, and so on.

Increased claim costs caused by social inflation may jeopardize insurance coverage affordability. Policyholders, insurers, and policymakers (legislators, courts, regulators, etc.) all play a crucial role in developing solutions-oriented conversations.

Be Prepared. It’s Affecting Your Bottom Line Already.

Social inflation occurs when one group of customers is charged low rates while others are charged high rates. When this happens, the profit margin on premiums for the low rate customers will be lower than the profit margin on premiums for the high rate customers. As a result, those low rate customers end up subsidizing the high rate customers while the company loses profit on the high rate customers.

Social inflation is the natural result of any risk transfer system that relies on a few people to bear the burden of risk while everyone else is protected by insurance policies that are priced too low. The trust the public is losing in businesses, specifically large corporations, lends to jurors finding defendants guilty at a larger volume which increases payout and increases costs.

If you want to reduce social inflation in your company, you’ll need to first understand how it happens. Once you understand the cause, you can take steps to reduce social inflation in your organization.

Key in all this is keeping claim costs as low as possible. One way to do this is automating your certificate of insurance (COI) tracking process. myCOI makes this process SO. SO. SIMPLE. We invented the space, and as such, have everything you need to erase the worry that tracking COIs can create.

Book your free, tailored demo today to see just how simple it can be!

The next uninsured third-party partner won't announce themselves.

illumend catches the gap.

You save the project.

Blog & Insights

What Are Policy Limits?

What Is Insurance Renewal Tracking?

What Are Insurance Requirements?

What Is an Insurance Exclusion?

Moving Beyond Spreadsheets to Manage Construction Risk

myCOI Launches illumendTM: Smart, Fast, Confident Compliance—Just a Click Away

Compete in a Crowded Industry with the Right Insurance Technology

General Contractors NEED Automated Certificate of Insurance Software

Has Your Organization Been Hurt By Insurance Claims?

Construction Industry Trends For Additional Insureds

.jpg)

How Insurance Agents Can Achieve Clients For Life

Get Your Team Off Your Back About COI Tracking

You Could Be Saving 30% on Insurance Tracking Costs

Tip# 1 – The “INSURED” Box

Constructing A Strong Contract

Are You Really an Additional Insured?

Insurance Agents: Watch Your Client Base Grow

What You Need to Know About Certs and Real Estate

Insurance and Cannabis: What You Need to Know

Create a Unique Agency Sales Strategy with myCOI

Important Steps for Managing Risk Using Your RFP

Cybersecurity and Remote Work: Managing the Risks

Blanket Endorsements: The ‘Am I Covered’ Checklist

10 Tips for Transferring Contractual Risk

myCOI Gives Back to the Community

A Guide to myCOI’s Go-To Insurance Resources

Here’s What You Need to Know About Example COIs

When You Need a Sample COI, Think ACORD

Here’s What You Need to Know About COIs

Insurance Compliance Will Be a Critical Role in 2022

.jpg)

Always, Always Remember that ACORD is not an Insurer

Agents: Your Insureds Deserve Automated COI Tracking

The Right Compliance Management Software is Crucial

The ABCs of Certificate of Insurance Compliance

A COI Template Will Only Take You So Far

The Importance of A Signed Contract

Checking More Than Just Expiration Dates

Dominate Your Insurance Agency Earning Power

Additional Insured Updates You Need to Know

Is COI the same as liability insurance?

The Basics of Quarterly Tracking

The Basics of Additional Insured Endorsements

What Is a COI in Contracting?

What Is A Certificate Of Insurance (COI) For?

Primary and Noncontributory Endorsement Form

7 Strategies for Managing Insurance Renewals

Fraudulent Certificates of Insurance Present Real Risks. Are You Prepared?

General Liability Certificate of Insurance

Certificate of Property Insurance

How to Check If a Business Has Insurance

How do I get an insurance certificate?

Customer Asking for Certificate of Insurance

How Do I Get a Certificate of Insurance in the USA?

The Basics: Waiver of Subrogation

What Is A Surety Bond and Why You Need One

You Need MORE Than Just Holding COIs

The Wrong COI is Just as Bad as No COI

It’s Easy to Create Your Own COI. Don’t Do it.

5 Things to Do to Verify Your COI is Valid

Finding a Certificate of Insurance Online is a Risk

Premiums Are On the Rise

A COI Example Can be a Great Guide—Or a Burden

Contractors Pollution Insurance

COI Real Estate

Broker Certificate of Insurance

Building Certificate of Insurance

What Is An LLC Certificate of Insurance?

Who Is Responsible for Subcontractors’ Work?

Do Contractors Need Insurance?

Construction Insurance Risk Management

Subcontractor Default Insurance: Everything You Need To Know

How Do You Calculate Building Construction Coverage?

What Is Regulatory Compliance in Construction?

What Is Not Usually Covered by Building Insurance?

What Is the Difference Between Property Insurance and Builders Risk Insurance?

What Is Considered a Third-Party Insurance?

What Is a COI in Construction?

Types of Construction Insurance

Why Is Builders’ Risk Insurance so Expensive?

What Is Builders’ Risk Insurance?

Third-Party Insurance Verification

Why Should I Outsource COI Tracking to myCOI?

Insurance Tracking Services

How Can You Track Insurance Policies?

What Is Insurance Certificate Tracking?

How to Ensure Contractor Compliance

myCOI Expands Procore Integration to Simplify Compliance and Payments

How Do I Generate a Certificate of Insurance?

Why Does a Company Need a Certificate of Insurance?

What Is an Insurance Certificate for a Business?

.jpg)

How Much Does a COI Cost in the USA?

How Important Is a Certificate of Insurance?

What Are COIs? A Guide To Certificates of Insurance

Agents: Help Contractors Manage Insurance Risks

What Is COI in Risk Management?

What Are the Five Elements of Risk Management?

What Is a Third-Party Risk Management System?

What Are the Key Elements of Third Party Risk Management?

Compliance in the Construction Industry

Third-Party Risk Management in Construction

You don't have to understand insurance to be good at insurance compliance.

With Lumie™, compliance is covered. So is everyone on your project.

Get The Lantern

.avif)